登陆

登陆题目详情

单选题 A portfolio manager has asked each of four analysts to use Monte Carlo simulation to price a path-dependent derivative contract on a stock. The derivative expires in nine months and the risk-free rate is 4% per year compounded continuously. The analysts generate a total of 20,000 paths using a geometric Brownian motion model, record the payoff for each path, and present the results in the table shown below.  What is the estimated price of the derivative

What is the estimated price of the derivative

学科:默认课程

时间:2025-12-27 14:16:21

相关题目

相关作业

题目1

题目1单选题

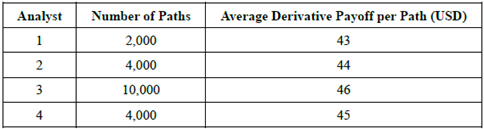

A portfolio manager has asked each of four analysts to use Monte Carlo simulation to price a path-dependent derivative contract on a stock. The derivative expires in nine months and the risk-free rate is 4% per year compounded continuously. The analysts generate a total of 20,000 paths using a geometric Brownian motion model, record the payoff for each path, and present the results in the table shown below. <img src="https://tihai-oss-cloud.itihey.com/img/6bc5c0bebb95a540afebd87a1758643f.png"> What is the estimated price of the derivativeA. USD 45.10B. USD 43.77C. USD 43.33D. USD 44.21

题目2单选题

Which of the following statements about Monte Carlo simulation is incorrectA. For estimating VaR, Monte Carlo methods generally require more computing power than historical simulationsB. Monte Carlo simulations can handle time-varying volatilityC. Monte Carlo methods can be used to estimate value-at-risk (VaR) but cannot be used to price optionsD. Correlations among variables can be incorporated into a Monte Carlo simulation

题目3单选题

Consider a stock that pays no dividends, has a vol. of 30% per annum, and provide an expected return of 15% per annum with continuous compounding. The stock price movements follow GBM. Consider a time interval of 1 week and the initial stock price is 100, then the stock price increase has a normal distribution withA. Mean = 0.268%, standard deviation = 4.03%B. Mean = 0.288%, standard deviation = 4.16%C. Mean = 0.288%, standard deviation = 4.27%D. Mean = 0.278%, standard deviation = 4.13%

题目4单选题

Consider a stock that pays no dividends, has a volatility of 25% per annum and an expected return of 13% per annum. Suppose that the current share price of the stock, S0, is USD 30. You decide to model the stock price behavior using a discrete-time version of geometric Brownian motion and to simulate paths of the stock price using Monte Carlo simulation. Let Δt denote the time interval used and let St denote the stock price at time interval t. So, according to your model, S_(t+1)=S_t×(1+0.13×∆t+0.25×√∆t×ε, where ε is a standard normal variable. To implement this simulation, you generate a path of the stock price by starting at t = 0, generating a sample for ε updating the stock price according to the model, incrementing t by 1, and repeating this process until the end of the horizon is reached. Which of the following strategies for generating a sample for Δ will implement this simulation properlyA. Generate a sample for ε by sampling from a normal distribution with mean 0.13 and standard deviation 0.25. Use Cholesky decomposition to correlate this sample with the sample from the previous time intervalB. Generate a sample for ε by using the inverse of the standard normal cumulative distribution of a sample value drawn from a uniform distribution between 0 and 1C. Generate a sample for ε by using the inverse of the standard normal cumulative distribution of a sample value drawn from a uniform distribution between 0 and 1. Use Cholesky decomposition to correlate this sample with the sample from the previous time intervalD. Generate a sample for ε by sampling from a normal distribution with mean 0.13 and standard deviation 0.25

题目5单选题

Monte Carlo simulation is suitable for pricing options in which of the following cases? I. An Asian option on a stock market index (payoff based on average stock price). II. A look-back put option on XYZ stock (payoff based on maximum or minimum stock price). III. An American call option on ABC stock (possible early exercise). IV. A cash-or-nothing call option (i.e., binary option) on SCU stock (payoff is fixed amount or nothing)A. I, II, and IVB. I and IVC. III and IVD. II and III

题目6单选题

A risk manager has been requested to provide some indication of accuracy of a Monte Carlo simulation. Using 1,000 replications of a normally distributed variable S, the relative error in the one-day 99% VaR is 5%. Under these conditionsA. Using 1,000 replications of a long option position on S should create a larger relative errorB. Using another set of 1,000 replications will create an exact measure of 5.0% for relative errorC. Using 10,000 replications should create a larger relative errorD. Using 1,000 replications of a short option position on S should create a larger relative error

题目7单选题

Suppose you simulate the price path of stock HHF using a geometric Brownian motion model with drift μ = 0, volatility σ = 0.14, and time step Δt = 0.01. Let St be the price of the stock at time t. If S0 = 100, and the first two simulated (randomly selected) standard normal variables are ε1 = 0.263 andε2 = -0.475, what is the simulated stock price after the second stepA. 99.97B. 96.79C. 99.70D. 99.79

题目8单选题

Which of the following statements about simulation is invalidA. When simulating asset returns using Monte Carlo simulation, a sufficient number of trials must be used to ensure simulated returns are risk neutralB. Bootstrapping is an effective simulation approach that naturally incorporates correlations between asset returns and non-normality of asset returns, but does not generally capture autocorrelation of asset returnsC. The historical simulation approach is a nonparametric method that makes no specific assumption about the distribution of asset returnsD. Monte Carlo simulation can be a valuable method for pricing derivatives and examining asset return scenarios

题目9单选题

The GARCH model is useful for simulating asset returns. Which of the following statements about this model is FALSEA. The GARCH imposes a positive conditional mean returnB. The GARCH can produce fat tails in the return distributionC. The Exponentially Weighted Moving Average (EWMA) approach of RiskMetrics is a particular case of a GARCH processD. The GARCH allows for time-varying volatility

题目10单选题

Suppose that the current daily volatilities of asset X and asset Y are 1.0% and 1.2%, respectively. The prices of the assets at close of trading yesterday were $30 and $50 and the estimate of the coefficient of correlation between the returns on the two assets made at this time was 0.50. Correlations and volatilities are updated using a GARCH (1, 1) model. The estimates of the model's parameters are α = 0.04 and β = 0.94. For the correlation ω = 0.000001, and for the volatilities ω = 0.000003. If the prices of the two assets at close of trading today are $31 and $51, how is the correlation estimate updatedA. 0.559B. 0.539C. 0.549D. 0.569

下载 题海APP

拍照搜题更快捷

- 海量题库

- 无搜索限制

- 快捷拍照搜题